On the morning of February 28, 2026, the joint US-Israel operation “Operation Epic Fury” launched strikes on Iran. Around 900 strikes hit in the first 12 hours. By the end of the day, Iran’s top religious and political leader Khamenei was dead; dozens of cabinet members, senior generals, and nuclear scientists were killed the same day. Even so, just a week later, a big chunk of the Western media was already running headlines saying, “the US is losing this war.”

A conflict where one side’s leader and dozens of top officials get killed on day one. How does the other side end up being called the winner?

This article looks at the economic side of the war — how Iran, the US, and the world economy were affected. And more importantly: who’s losing, who’s winning? Not from the media’s frame. From the numbers.

Before the War Started: Iran Was Already Sinking

To understand this war properly, you first need to understand the shape Iran was in when it walked into it.

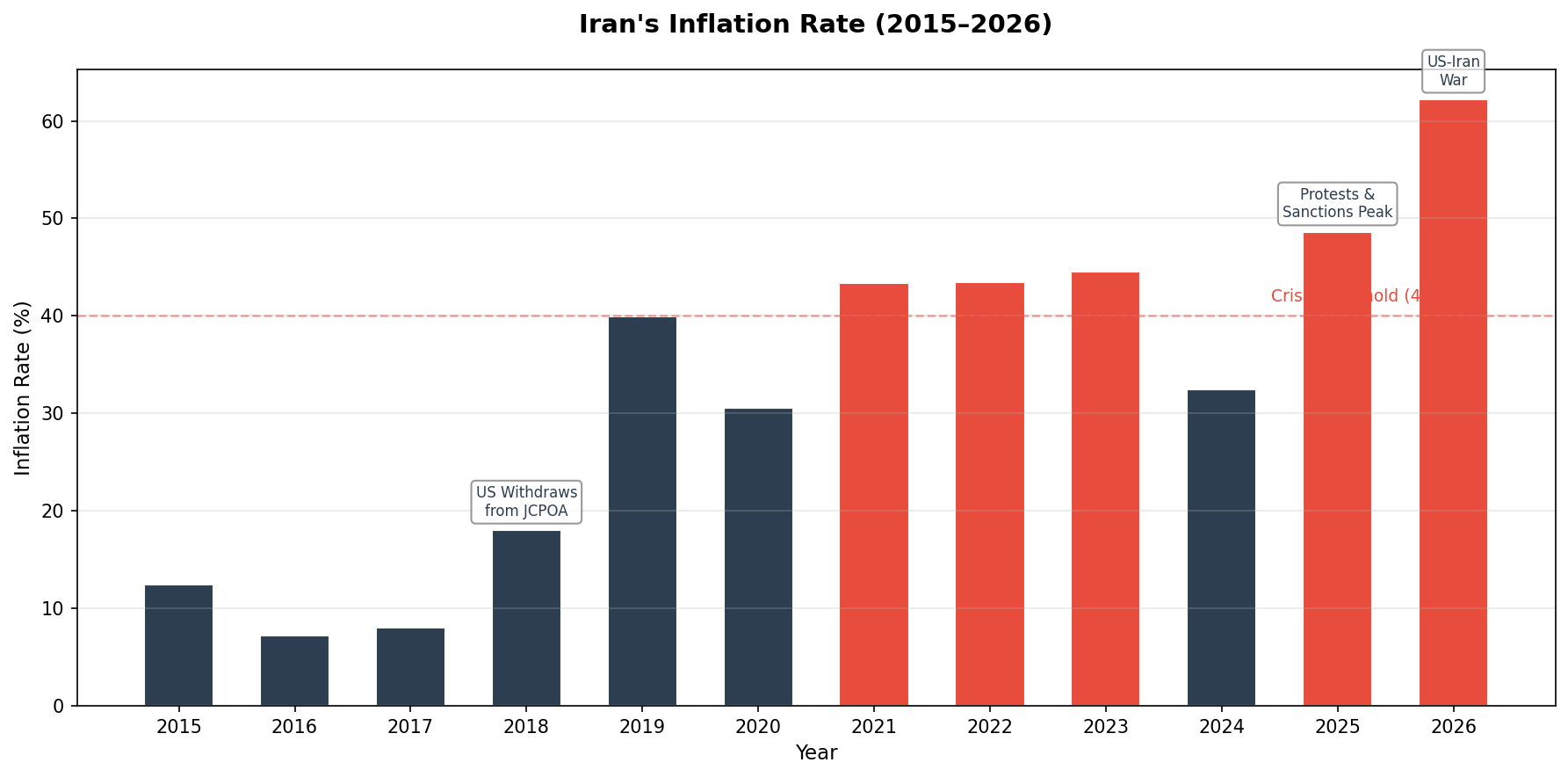

Iran’s economy peaked in 2012 at around $644 billion. By 2025 it had dropped to $356 billion — an economy almost cut in half. Behind it: sanctions, chronic governance crises, and structural problems.

The story of the rial is even more striking. Before the 1979 revolution, one dollar got you about 70 rial. By March 2025, one dollar passed one million rial and the rial took the title of the world’s least valuable currency. By the time the war started, the rate was near 1.75 million.

The chart tells this story clearly. The climb that started with the US pulling out of the JCPOA in 2018 never reversed — it held its levels for years, picked up after the 12-Day War, and by 2026 food inflation hit 99 percent. During the war, Iran’s central bank had to put the largest banknote in its history — 10 million rial — into circulation. According to people close to the government speaking to Reuters, officials are worried they won’t be able to cover salaries in the short term unless a ceasefire is reached.

The World Bank had projected, before the war started, that Iran’s economy would shrink by 2.8 percent in 2026. On top of that, the Iranian government has put the damage to its own economy at a minimum of $300 billion, possibly as much as $1 trillion.

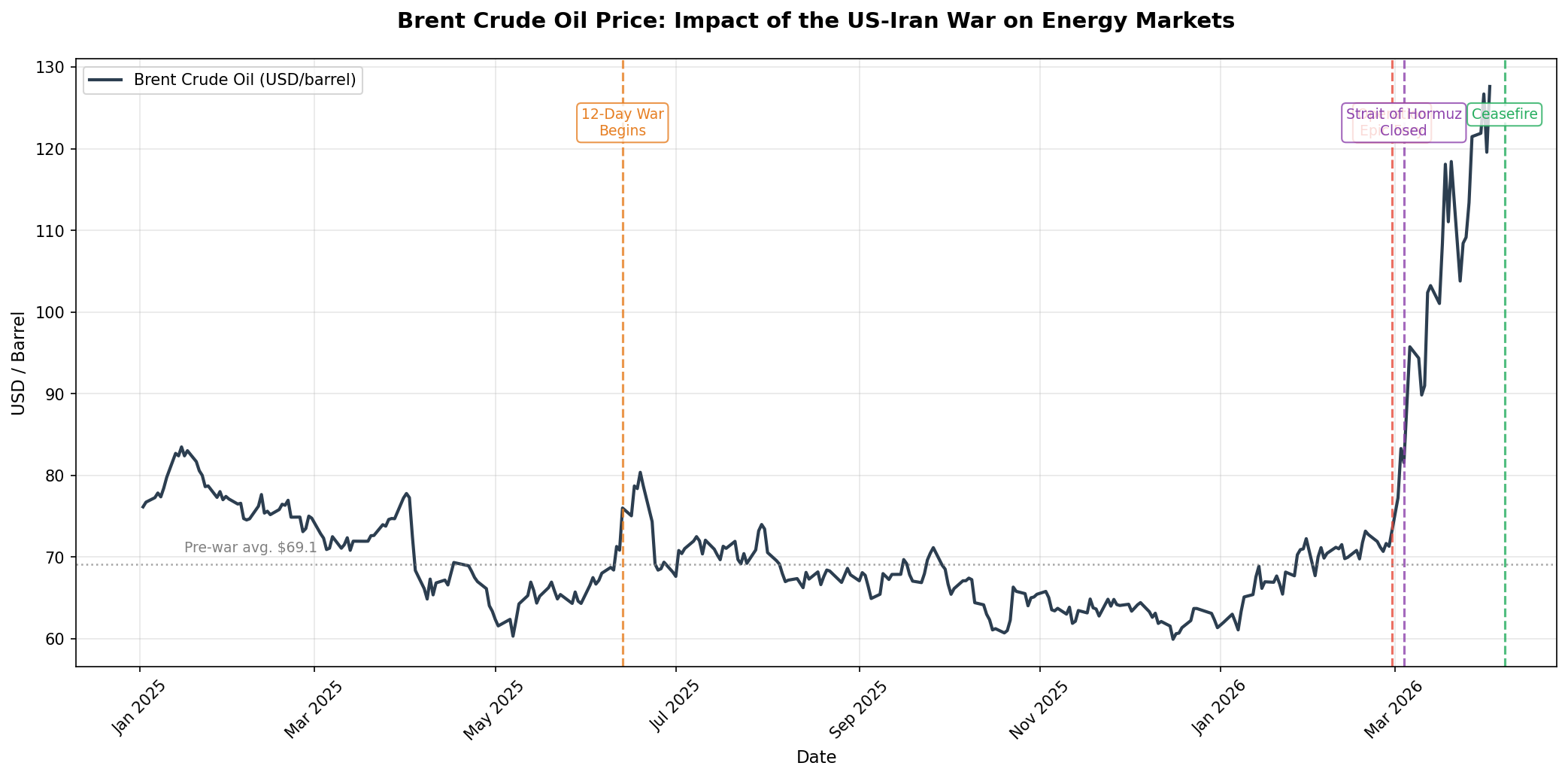

For all of this, Iran has one strong card in its hand: the Strait of Hormuz. It didn’t close the strait to everyone. It went selective — its own ships, ships paying transit fees, and ships from countries that struck a deal. Commercial traffic through the strait dropped by over 90 percent in March, and there’s an irony in this strategy: thanks to rising oil prices, Iran pulled in an average of $25 million a day in extra oil revenue in March.

Is the US Really Losing?

That the US is taking economic damage from this war is a given. But “taking damage” and “losing” aren’t the same thing.

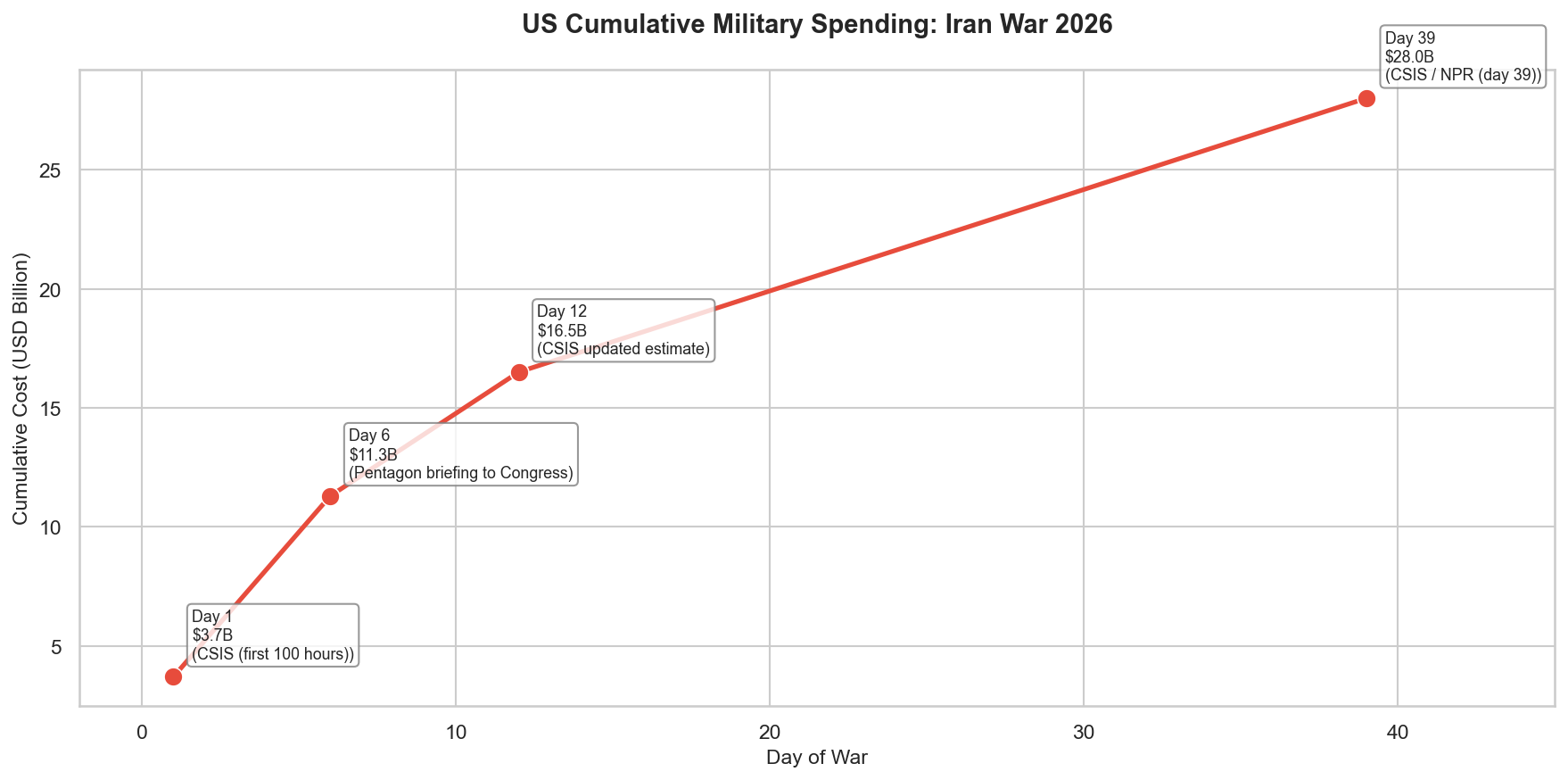

According to the Pentagon’s briefing to Congress, the first 6 days of the war cost $11.3 billion. By Day 12 that figure had hit $16.5 billion. The Pentagon has asked Congress for a $200 billion supplemental. For comparison: the Iraq War was initially projected to cost $200 billion. The actual cost ran into the trillions.

But here’s where you have to draw a line. For a $28 trillion economy, $16–95 billion is a manageable load. The real cost is somewhere else.

The least talked about but most critical military side of this war is this: in the first 100 hours, Iran fired more than 2,000 drones and over 500 ballistic missiles (CSIS). The US shot them down with Patriot and THAAD interceptors. The cost ratio is striking — on average 106 times the cost of the drone per interceptor. Besides the costs, one of the other problems is that these missiles can’t be made overnight. By the end of March, the Pentagon had to sign a deal with Lockheed Martin and BAE Systems to quadruple the annual production of THAAD components. Stockpiles are running out. And this directly affects the air defense capacity that NATO, Taiwan, and Ukraine are counting on the US for.

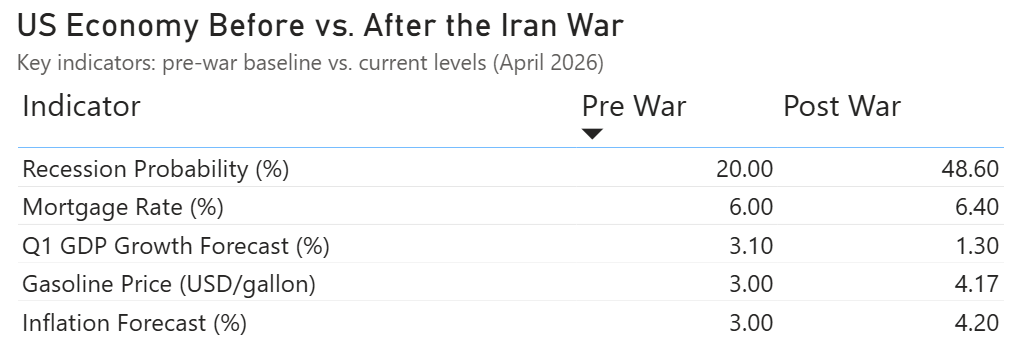

On the economic side: growth forecasts came down, gas prices went up, recession expectations climbed. One nuance matters here: the US, thanks to the shale revolution, is now close to being a net energy exporter. The country gets a slight benefit from the rise in global energy prices. Energy companies win; consumers lose. The distribution is uneven — but compared to a country like Japan or South Korea, the US position is fundamentally different.

The real issue isn’t the scale. The lack of strategic clarity and the damage to alliances are the items on the actual bill.

The Rest of the World: Where Are the Real Victims?

To understand the global impact of this war, you need a bit of historical context first.

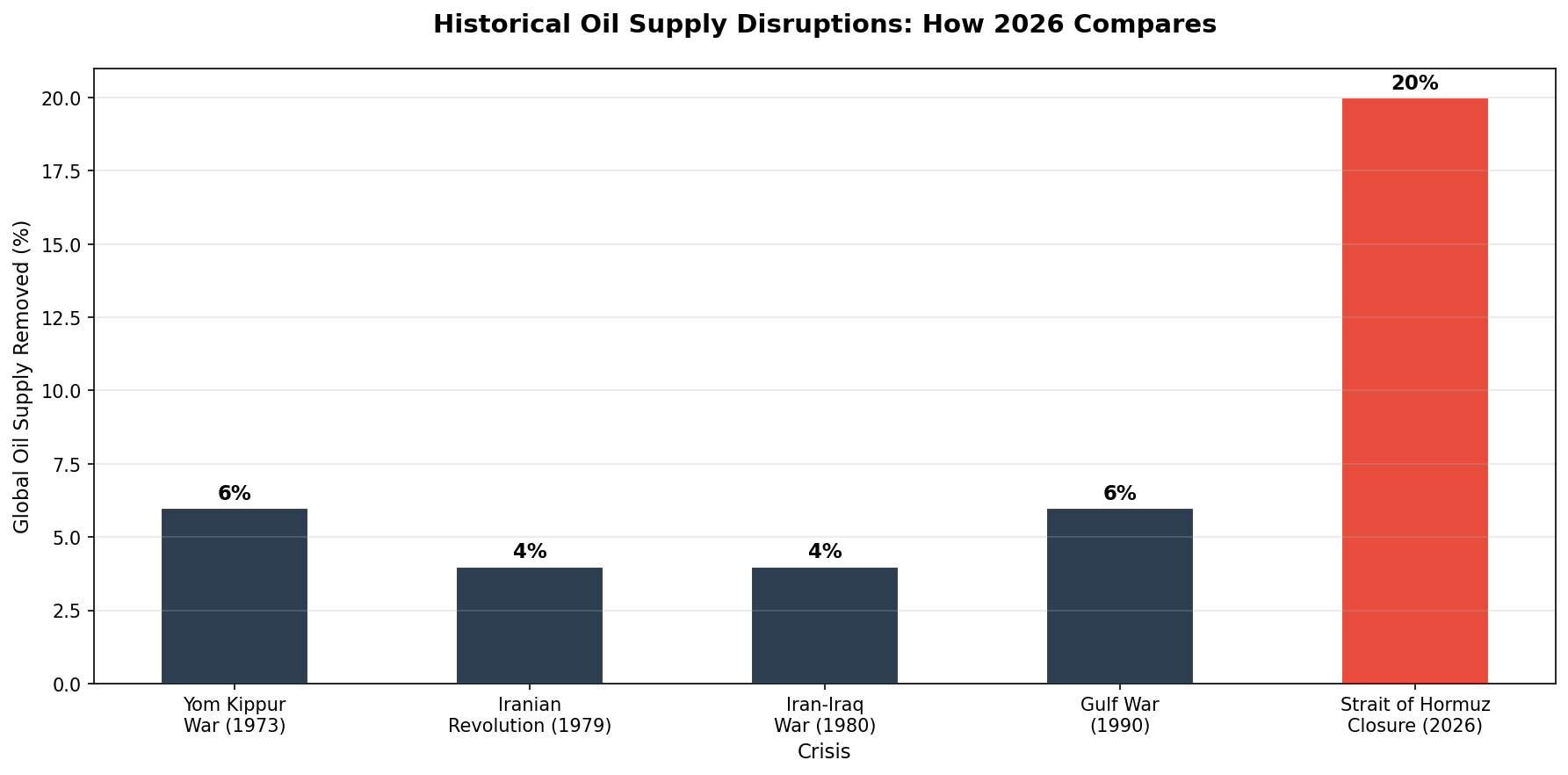

1973, 1979, 1990 — in the great oil crises of history, the volume pulled out of the market stayed within 4 to 6 percent of global supply. In 2026 that ratio hit 20 percent. The IEA called it “the largest supply disruption in the history of the global oil market.”

But this war isn’t just an oil crisis. Qatar’s Ras Laffan LNG facility took serious damage from an Iranian strike, and repairs will take 3 to 5 years. A big chunk of the raw materials that go into global fertilizer production passes through Hormuz, hitting agricultural costs directly and feeding into food prices. A meaningful share of helium — which plays a critical role in semiconductor manufacturing and medical imaging — also comes from the same region. So this crisis went beyond energy markets; it hit several critical points in the supply chain at the same time.

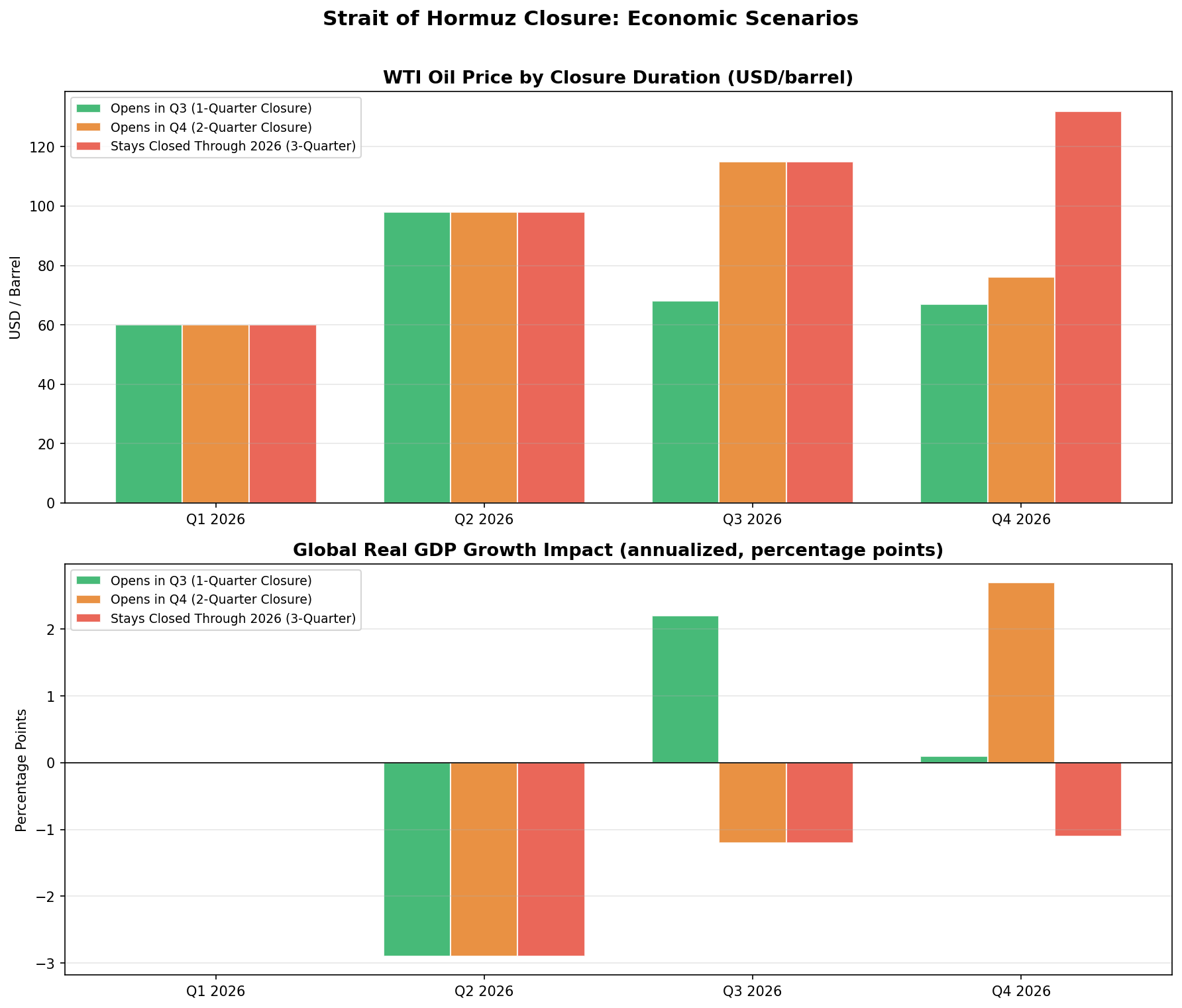

According to the Dallas Fed model, a closure of Hormuz through the second quarter pulls global growth down by an annualized 2.9 points. If the closure runs three quarters, oil hits $132 a barrel by year-end.

What the chart shows is that the longer the strait stays closed, the more the impact compounds. And there’s a fact being overlooked here: tankers loaded before the war take 4–6 weeks to reach port. Some of the cargo that left before the strait closed still hasn’t arrived. Once that inventory runs out, the futures market price will have to converge with the physical price. Meaning: even if a ceasefire is announced, prices won’t drop right away.

Europe

Europe is going through its second major energy crisis. The continent went into this crisis unprepared, closing winter with historically low gas storage levels. The central bank pushed back its rate-cut plans, growth forecasts were revised down, and energy-intensive industries are facing cost pressure.

Asia

Asia is the region most directly affected. Almost all of Japan’s oil comes from the Middle East. Some countries’ oil reserves only cover a few weeks of demand. Fuel queues, university shutdowns, emergency declarations — that’s what this crisis looks like in the region day by day.

The Gulf

In the Gulf, the picture is much more dramatic. A large portion of food imports have been disrupted, drinking water systems are under threat. The “safe investment hub” image these countries built over the last few years — the new model Dubai and Doha built around tourism and finance — may have been shaken beyond repair.

So, Who’s Winning, Who’s Losing?

The two sides of the table are clear.

Net Losers

The Iranian people are the biggest losers of this war. Already carrying the heavy weight of decades of sanctions and governance crises before the war, the Iranian people came out the other side with a hardened regime and a much worse economy. The regime didn’t change — if anything, the IRGC’s weight grew.

The Gulf states took over $120 billion in damage. Japan, South Korea, and Southeast Asia were directly hit because of their oil dependence. Europe got caught in its second energy crisis.

Net Winners

Russia is the side pulling the most concrete economic gain from this war — an average of $150 million a day in extra revenue in March. But the real profit isn’t a few hundred million dollars. The US having pulled some of its focus away from Ukraine, the weapons that didn’t get sent to Ukraine, a weakened NATO — those are Russia’s real gains. At a time when Western sanctions were starting to bite for the first time, the war loosening those sanctions worked in Russia’s favor.

Defense contractors are also among the war’s winners. Raytheon and Lockheed Martin pushed their production to — in Trump’s own words — “a speed never seen before.” Net energy exporters like Norway and Canada also gained from the higher prices.

The Complicated Picture: China

China can’t be summed up in a single sentence. In the short term, China is taking damage: oil purchases from Iran have been cut off, Gulf-sourced supply has been restricted. According to the Bruegel model, a 25 percent rise in oil prices pulls Chinese GDP down by about 0.5 points.

But China was prepared. It stockpiled before the war and has roughly four months of strategic reserves. And most importantly: some Chinese-flagged ships are reportedly being granted passage through Hormuz — Iran has opened a special corridor for China.

China’s real fear isn’t energy, it’s exports. Europe takes 15 percent of China’s exports. If Europe goes into recession, Chinese exports drop, corporate profits shrink. On the other hand, in the longer term, some analysts argue that the US having its attention pulled off the Pacific and losing global standing creates a geopolitical opening for China.

The Complicated Picture: The US

Former CFR president Richard Haass asked the question in week 5 of the war: “Are you better off than you were five weeks ago?” And he answered it: “Absolutely not.”

The tactical wins are real: Khamenei was killed, nuclear infrastructure was hit, Iran’s naval forces took serious damage. But the strategic objectives didn’t materialize. The regime didn’t change — it hardened. Hormuz still isn’t fully open. The US’s own intelligence reports indicate the nuclear sites weren’t fully collapsed, and that Iran moved a significant amount of enriched uranium out before the strikes.

That said: for a $28 trillion US economy, the direct spending on this war is a manageable load. The rise in gas prices hits consumers but doesn’t break the economy. The real bill is piling up in the interceptor stockpiles emptying out for the Pacific, the cracks forming in NATO, the relationship with Europe that’s gone south — basically, in the items you don’t pay for in dollars.

Where Does the “Iran Is Winning” Narrative Come From?

Iran’s war strategy was never aiming for a military victory. In the words of international relations scholar Robert Pape, it was “horizontal escalation” — widen the war, spread out the economic and political cost, make it unsustainable. The Hormuz card made it possible. A much weaker country, by controlling a single strategic chokepoint, was able to paralyze the global economy.

That’s real. And that doesn’t mean Iran “won.”

The “US is losing” narrative is fed partly by an over-reading of that reality, partly by the attention economy of the media. The dilemma of the strong always reads better. But when you look at the data, the picture is different. Iran’s GDP got cut in half, its currency became the world’s least valuable, its nuclear infrastructure was hit, its leader was killed, and its economy — by its own admission — took between $300 billion and $1 trillion in damage. Calling that “winning” doesn’t line up with the numbers.

The real losers of this war should be read from the numbers, not the media. And those numbers say: the people taking the most damage are the Iranian people, the Gulf states, Asia’s energy-dependent emerging economies, and Europe.

The economic story of this war isn’t over. Until Hormuz opens, nothing goes back to normal. Repairing Qatar’s LNG facility will take 3–5 years. The Gulf’s safe investment hub image has been shaken. As Steve Hanke pointed out in Fortune, the first serious cracks have started showing in the petrodollar system. These are wounds that won’t close with a ceasefire.

Sources: Federal Reserve Bank of Dallas (March 2026); CSIS — Cancian & Park, “Iran War Cost Estimate Update” (March 2026); U.S. Congressional Research Service R48887 (March 2026); Defense News — THAAD production agreement (March 2026); Bloomberg — Dallas Fed Hormuz analysis (March 2026); World Bank Iran Macro Poverty Outlook (March 2026); IMF World Economic Outlook (October 2025); IEA Strait of Hormuz statements; Bruegel — “China and the 2026 Iran war” (March 2026); Richard Haass / Project Syndicate (April 2026); Fortune / Steve Hanke (April 2026); Britannica “2026 Iran war”; Wikipedia “Economic Impact of the 2026 Iran War.”